By Christopher Vecchio, Currency Strategist

Fundamental Forecast for Euro:Neutral

- EURUSD appears to have made a significant turn on the charts…

- …and recent gains seen in EURUSD may be setting up a ‘sell the rally’ opportunity.

- Have a bullish (or bearish) bias on the Euro, but don’t know which pair to use? Use a Euro currency basket.

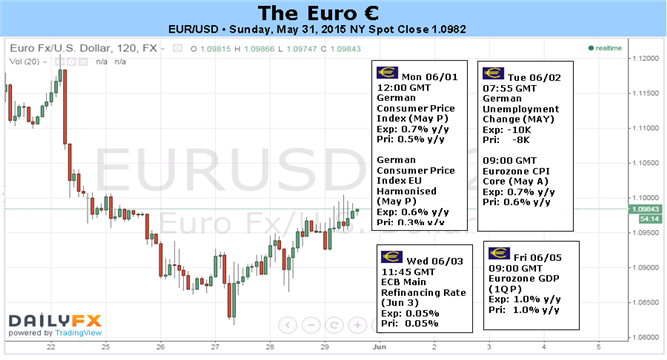

While EURUSD

was pressured into fresh monthly lows just above $1.0800, a late-week

rally in the EUR-crosses wiped out nearly all losses accumulated earlier

across the spectrum. Dodging disparaging headlines about Greece’s

ability to reach consensus with her creditors, EURUSD only closed -0.10%

lower at $1.0990, while EURAUD and EURJPY led the EUR-crosses higher by +2.22% and +2.02%, respectively.

The Euro’s sensitivity to the situation in Greece is

bound to jump in the coming days, even if only temporarily, as a June 5

deadline for a payment to the IMF looms. This is a delicate situation

insofar as the Greece government is purportedly open to defaulting on

her obligations in order to maintain its political party’s pre-election

promises. As far as the impact of the intraday headlines on the Euro,

the likelihood remains low; but the ever so important tail risk scenario

is becoming more probable, likely to leave traders a bit uneasy.

Of course, in the background, the ECB’s QE-driven

trade – via the portfolio rebalancing channel effect – is dictating

asset performances across the risk spectrum. In tandem, European

sovereign yields are falling, the Euro is depreciating, and European

equity markets are rallying (or vice-versa). This trilateral

relationship should continue to persists, irrespective of the Euro’s

direction.

In the very near-term, there is heightened risk to

the Euro (and more specifically, EURUSD) as a calendar packed with

medium- and high-ranked event risk is on the horizon. Event-driven

volatility – particularly between the hours of 08:30 GMT to 14:00 GMT –

will be well-represented this coming week.

On Monday, the German Consumer Price Index for May

and the May US ISM Manufacturing survey are due. On Tuesday, May German

labor market data and the May Euro-Zone CPI will be released, as well as

US Factory Orders for April. On Wednesday, the ECB will hold its June

interest rate meeting and press conference, while the May US ADP

Employment Change report, the May US ISM Services gauge, and the Fed’s

Beige Book will be released. On Thursday, the May PMI readings for the

Euro-Zone and Germany, and the weekly US jobless claims data will be

released. Lastly, on Friday, Q1’15 Euro-Zone GDP data will be released,

while the May US Nonfarm Payrolls report and unemployment rate wil be

due.

Needless to say, there are items on the calendar

over the next few days on both sides of the pond that are likely to

increase volatility around EURUSD. Besides previously discussed

influences lingering in the background – Greece and the ECB’s QE program

– the one theme that will be put to the test this week, that could

drive the direction of EURUSD for the coming weeks, will be the notion

that the US economy has reversed its early-year slowdown. Only if the

recent optimism over the US growth story in Q2’15 is confirmed by the

upcoming data, will the rising interest rate differentials in favor of

the US Dollar

story take hold. By the end of the week, we should have a better idea

of which way EURUSD will be trading for the foreseeable future. –CV